ZINSURANCE |

|

A blog to help you prepare for life's unexpected

|

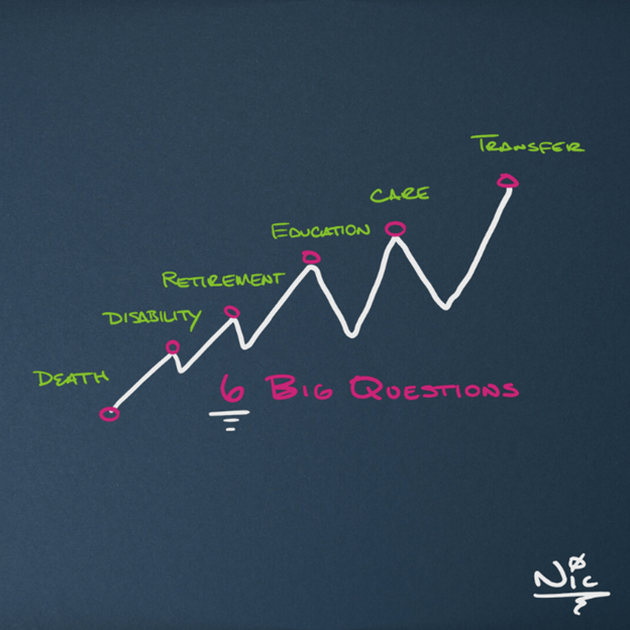

It is my pleasure to welcome Nic Nielsen with Know My Plan as our second guest blog contributor. Nic has always been on the forefront of financial planning since I met him 15 years ago when he was the first in the territory to offer easy issue simplified underwriting. I appreciate his deep understanding of insurance as a financial tool. Nic thrives on learning, understanding, and analyzing everything beforehand to affirm it is the right and best option. I admire his patience and ability to listen and relate to each client. In this blog, he focuses on the simple truth of financial and estate planning centered around 6 Big Questions. - Lori  One of my biggest pet peeves about the financial planning industry is the desire to make the process sound complicated. It isn’t complicated. It comes down to six key life factors around how you should financially plan for your death, potential disability, retirement, children’s education, your care as you age, and transferring your wealth. Asking questions around these six key aspects should always be your financial plan’s starting point. Often, the answers become siloed. The CPA, estate planner, investment manager, financial planner, and insurance advisor must all be on the same page for optimal results. Financial planning is often only as strong as its weakest link. A beautiful investment strategy can be derailed by not planning for long-term care. Carefully crafting Roth conversions to minimize taxes throughout your lifetime can be offset by a permanent disability. Not only is a financial planner's job to listen to your desires and succinctly answer the questions around these six key factors, but to make sure that all of these answers are coordinated for you with all within your advisory team. Taking Action Early  A husband and wife had recently relocated to the Charlotte area with a child and a big lovable dog. The husband, a 40-year-old executive at a large corporation, knew that they needed some guidance. Finding a guide became a high priority with a new job, scattered investment accounts, old retirement plans, and a lack of time. With their free time, they wanted to spend it as a family. Their dreams identified in our first meeting included living in the mountains, playing guitar, watching hockey, and eating good Thai food). Together, we came up with a best-case guess of how much it would cost monthly to fund this life today. This is where I get to geek out on math and figure out how much this couple needs to fund their best life. We leverage getting the number through time value of money calculators and then adjust for inflation. After diving into their financial situation, there were some gaps. The vast majority of financial planning comes down to answering 6 big questions. This is where we always start. Are there additional questions that come up during the planning process? Yes, but most of the time, they are derivatives of the Big 6. The Big 6 Questions You Should AskThe Big 6 Questions below share how we approached working with this family, in their specific plan. These are questions you should consider for your own family’s approach to planning.

When it comes to financial planning, it’s simple, but not easy. For Your Future, Nic Nic Nielsen, CFP® BIO: Nicholas Nielsen, co-founder of Know My Plan, is a Certified Financial Planner who helps busy executives reduce financial stress and anxiety for themselves and their families with a one-page plan. Nic believes financial planning doesn't have to be overly complicated and you don't have to do it alone. He enjoys working with clients who want to build a financial plan together thru a deep understanding of their goals both while working, in retirement, and beyond. Inspired by his philosophy that many financial planning topics are better told with a picture, Nic is the author of Visual Finance, a book that contains 40 sketches by Nic along with 40 QR codes that link to short videos to illustrate real-life financial planning insights and applications. He earned his bachelor degree in Business Administration with the University of Saint Francis, where he played collegiate baseball.

0 Comments

Leave a Reply. |

About the BlogHi, I’m Lori Capozza Zeind, Archives

April 2023

Categories |

RSS Feed

RSS Feed